Why is there a need to have adjusting entries?

Accounting works under an accrual basis, which ensures to record things exactly when they happen, so an accountant would:

- Record assets at the time those resources are obtained

- Record liabilities at the time those obligations occur

- Record revenues at the time goods and services are provided to customers– Revenue recognition principle

- Record expenses at the time costs are used in running the company– Expense recognition principle

However, since cash flows can occur at a different time when revenues/expenses are recognized, we need adjusting entries– record any so-far unrecognized revenue or expense, as a means of updating balances of accounts when there are timing differences between cash flows and the recognition of revenues and expense. Adjusting entries are recorded at the end of an accounting period (such as Dec. 31).

What are examples when cash flows occur before revenues/expenses are recognized?

Cash flows can either occur before or after revenues and expenses are recognized. The two ways cash flows occur before revenues and expenses are recognized are prepaid expenses (asset) and deferred revenues (liability).

Prepaid expenses occur when a company pays cash to purchase in advance of using the asset ("buy now use later"). Prepaid expense accounts are thus assets because they show what a company has and can use. Examples include prepaid rent, prepaid insurance, supplies and equipment. In cases of prepaid expenses, there is an initial transaction for the purchasing of the prepaid asset that debits the asset bought and credits the payable account (amount we owe). Then there is a second transaction for when the asset is actually used up, and it credits the asset (because it is used up) and debits the expense; this is the adjusting entry. For example:

Journal |

Nov 31: $23k worth of supplies is bought on account | Nov 31 Debit Credit Supplies (+A)........................................................................$23k Supplies payable (+L)........................................................................$23k Operating activity (here, assets were obtained) |

Dec 31: $10k worth of supplies is used up for month | Dec 31 Debit Credit Supplies expense (+E, -SE)….……………………………….$10k Supplies (-A)...……………………………………………………………$10k Operating activity (adjusting entry) |

Deferred revenues occur when cash is received from customers in advance of services to be provided. Deferred revenue accounts are thus a liability because they show the amount of service a company owes. There is an initial transaction for the purchasing of the service and it debits cash and credits deferred revenue (a liability account because the company owes a service). The second transaction for when the service is actually provided, and it debits the liability and credits revenue because the service has now been provided; this is the adjusting entry. For example:Journal |

Dec 23: Company receives $6k from customers for soccer training to be provided later | Nov 31 Debit Credit Deferred revenue (+L.).......................................................................$6k Cash (+A)..............................................................................$6k Operating activity (here, cash was obtained) |

Dec 31: Company provides $6k worth of soccer service | Dec 31 Debit Credit Service revenue (+R, -SE)……………...……………………………….$6k Deferred revenue (-L).....………………………………………$6k Operating activity (adjusting entry) |

What are examples when cash flows occur after revenues/expenses are recognized?

The two ways cash flows occur after revenues and expenses are recognized are accrued expenses (liability) and accrued revenues (asset).

Accrued expenses occur when a company incurs costs, such as salaries, by the end of the current period but will not pay until the following period. Accrued expense accounts are thus a liability because they shows how much a company owes for incurred costs. Common examples are salaries payable, utilities payable and interest payable. The adjusting entry occurs first (on the last day of the period). This first transaction will debit expense because expense actually arises, and credit the accrued expense account because company actually starts owing something. The second transaction comes in the new period, and it credits cash because the company has now actually paid, and it debits the accrued expense account because the company no longer owes anything.

Journal |

Dec 31: Workers earn $3k worth of salaries from 28th-31st, but company won’t pay until Jan 4 | Dec 31 Debit Credit Salaries expense (+E, -SE)..................................................$3k Salaries payable (+L).........................................................................$3k Operating activity (adjusting entry) |

Jan 4: Company pays off $3k | Jan 4 Debit Credit Cash (-A).............................................................................................$3k Salaries payable (-L)..............................................................$3k Operating activity |

Accrued revenues occur when a company provides goods and services but has not received cash. Accrued revenue accounts are thus an asset because they show how much a company technically has but has yet to receive. A common example is accounts receivable. Once again, the adjusting entry occurs first (on the last day of the period). This first transaction shows when the company actually provides the service, at which point it credits service revenue and debits accounts receivable. The second transaction occurs in the next period when the customer actually pays the customer, at which point it credits accounts receivable but debits cash. For example:Journal |

Dec 31: Company offers soccer training but customers will pay $20k later | Dec 31 Debit Credit Accounts receivable (+A)......................................................$20k Service revenue (+R, +SE)................................................................$20k Operating activity (adjusting entry) |

Jan 8: Customers pay off all $20k worth of training | Jan 8 Debit Credit Cash (+A)...............................................................................$20k Accounts receivable (-A)....................................................................$20k Operating activity |

What happens after adjusting entries are recorded?

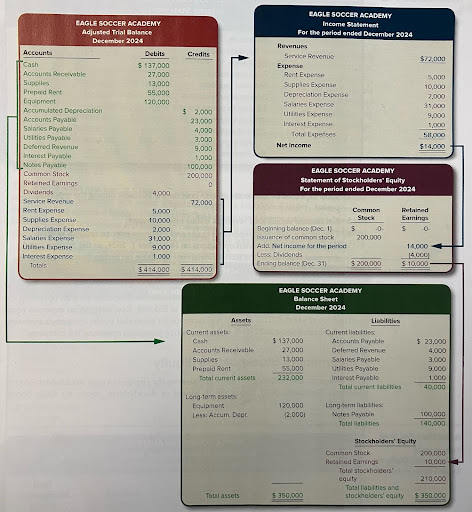

After adjusting entries are recorded, accountants adjust the general ledger and trial balance. The following are the adjusted version of the general ledger and trial balance from the "Recording Transactions" page:

These post-adjustment values can then be used to finalize the main financial statements used for communication.Now, as of the accounting period end of Dec. 31, the revenue account, expense account and dividend account will still have positive amounts. However, these three accounts are temporary accounts– balances are transferred into retained earnings and then those accounts’ balances become $0. Thus, we need closing entries– used to transfer balances of all temporary accounts to the balance of the retained earnings account. Using the above balance sheet, we will have the following closing entry:Journal |

Dec 31 | Dec 31 Debit Credit Service revenue (-R, -SE)...........................................................$72k Retained earnings (+RE, +SE).....................................................................$72k

Rent expense (-E,+SE)..................................................................................$5k Supplies expense (-E, +SE).........................................................................$10k Depreciation expense (-E, +SE)....................................................................$2k Salaries expense (-E, +SE)..........................................................................$31k Utilities expense (-E, +SE).............................................................................$9k Interest expense (-E, +SE).............................................................................$1k Retained earnings (-RE, -SE).......................................................$58k

Dividends (-D, -SE).......................................................................$4k Retained earnings (+RE, +SE).......................................................................$4k |

What about the statement of cash flows?

Among all four cases of timing differences in cash and revenue/expense recognition, there are no adjustments to the cash account at the end of the accounting period (Dec. 31). This is because for prepaid expenses and deferred revenues, cash is not changed in the adjusting entry; and for accrued revenues and accrued expenses, cash is changed in the second transaction that takes place in the next accounting period. Thus, to create the statement of cash flows, we only need to consider the standard transactions. In the "Recording Transactions" page, there were 10 company transactions, some of which had cash flows involved:

Accountants then record each of the activities with cash involved onto the statement of cash flows.

The final amount in the statement of cash flows should match the cash account balance on the balance sheet.